Share on:

Blockchain technology is the direct translation of the concept of value creation chains (Value Creation Network), this revolutionary technology provides a new concept to prove any type of transaction that requires financial movement, transfer of physical or intangible asset or order procedures and the subsequent approvals. This technology not only provides easy and accessible solutions to these transactions, but also goes beyond them to give these transactions reliability and security standards that cannot be denied or circumvented.

Due to the abundance of information on this topic, we will discuss this technology in three consecutive episodes. We will start here by talking about this technology and describing its service structure and main features.

Blockchain technology was invented in 2008 by a person or group of people under the name (Satoshi Nakamoto – and this identity is still unknown and unknown until now – and this technology was relied on to design the first cryptocurrency digital currency, “Bitcoin”.

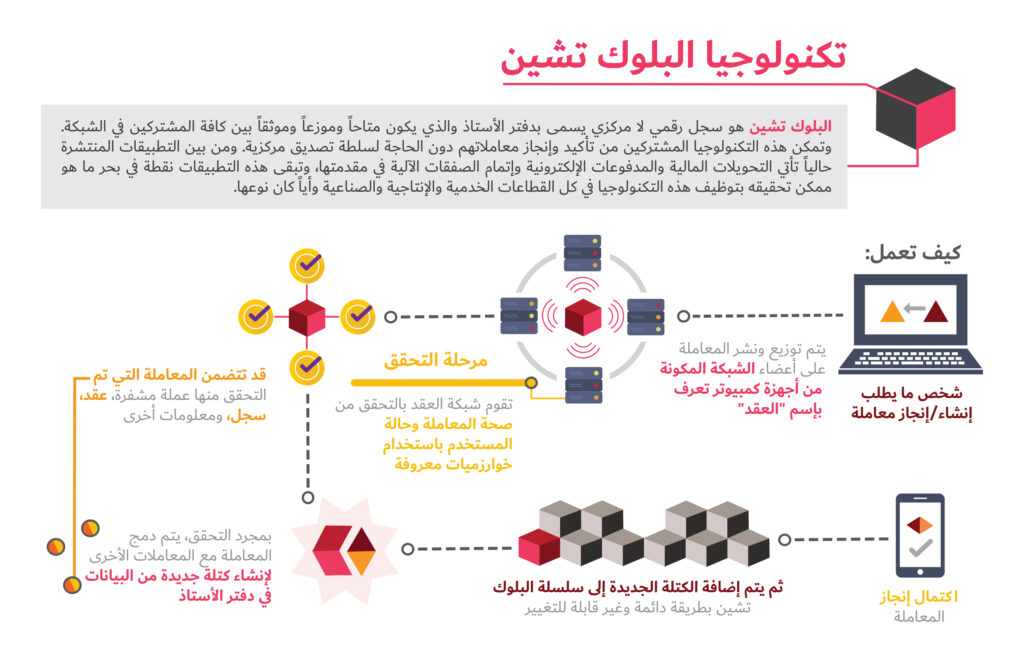

Blockchain can be defined as a distributed database that resides on multiple computers at the same time. The blockchain database consists of a set of blocks that contain digital records, and each block holds special encryptions for the time dates in which it was created, and links to the previous block, and in this way a chain of blocks is formed with new additions, and the data of these blocks can only be modified by agreement The parties involved in the network.

Blockchain technology has enabled a solution to the problem of duplication that usually occurs in electronic records; Repeated spending of the same amount of money in different locations, for example. This is due to the structure of the system in securing, documenting, keeping records, and sharing data with all connected parties on the network, in addition to the complex encryption degrees and security standards used. All of this, in turn, stimulated the development of smart applications based on blockchain technology, especially in enabling the emergence of cryptocurrencies and their uses in the world.

Blockchain technology is primarily an organizational and management concept for financial and commercial transactions. The developers have provided different solutions to implement this concept, and these solutions differ from each other in terms of details and specifications, and these solutions come as operating platforms that allow their subscribers to carry out their transactions through them, and also allow programmers to implement complementary solutions to the needs of institutions or in the design of detailed services that require a high degree of accuracy, reliability and reliability.

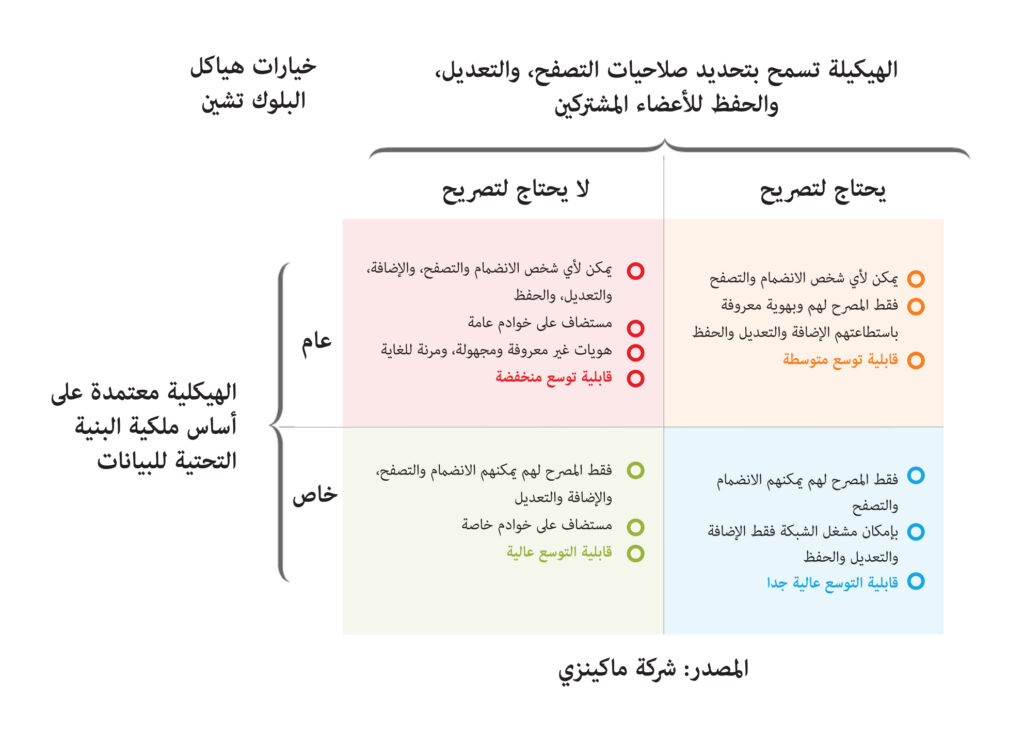

Blockchain service platforms can be classified into two basic categories:

1- Public Platforms: This category of platforms is called Permission-less Platforms, as it does not require knowledge of the subscriber’s identity, and its users can use pseudonyms. One of the most famous of these platforms is the Bitcoin platform, which is completely open to the public, and subscribers can open accounts and digital financial wallets, exchange currencies, and practice mining activities for cryptocurrency (Cryptocurrency Mining) without revealing their real identities. (*Mining is a term that refers to the procedures by which electronic transactions containing cryptocurrency are documented and digital records are added to the blockchain base).

One of the disadvantages of open platforms is that they are slow and consume a large amount of energy, in which the time to complete a transaction may reach more than 10 minutes. These networks are characterized by automatic control of the system, which depends on the consensus of a large number of subscribers or work points (nodes) on electronic operations. Among the most popular public platforms are:

a. Bitcoin (Bitcoin): It is the main platform for the transfer of Bitcoin, buying and selling. The market value of the platform is currently estimated at more than 180 billion dollars, where the price of one coin exceeds 10 thousand dollars and a basket of currencies reaches 17.8 million coins, and about 1,800 new coins are mined daily.

b. The Ethereum platform: It is used in various applications, including the Ethereum currency and smart contracts, and is considered extensive in terms of scalability, and is characterized by being able to function as a private platform as well.

c. Stellar platform: It provides fast and efficient solutions for financial institutions and individuals, especially in the field of payments and money transfers, that are fast and reliable, and at almost no additional cost. The platform also enables developers to create electronic wallets with mobile applications and use smart banking tools to develop online payment systems. The platform is also distinguished by being able to function as a private platform.

2. Permissioned Private Platforms: These platforms provide work environments for developing smart applications that suit the requirements of institutions, government and private agencies. These platforms only allow those concerned with real identities, which are approved by the owners of these platforms. It also requires internal approvals and multiple regulatory procedures, which are usually programmed within the mechanisms of the electronic work system and to comply with legal and procedural requirements; That is, transactions must be approved by specialists and authorities, or through algorithms that can be developed on demand, and according to the technologies of each platform separately. Among the most famous private platforms, in addition to some of what has been mentioned, are:

a. Hyperledger Fabric: Provides a framework for developing smart technology applications such as smart contracts, finance systems, supply chain management systems, and manufacturing. Companies such as IBM have invested in this platform to build smart applications and services for enterprises.

b. OpenChain: OpenChain is a highly secure, open source ledger technology platform developed by Coinprism for organizations that want to manage and maintain their digital assets.

c. Ripple: The platform is known for bringing together payment providers, banks and businesses and as the best platform for developing cross-border payments solutions. The platform is suitable for large enterprise use and less suitable for small and medium businesses or individual users.

Perhaps the most important feature of these platforms is their ability to enable developers to build applications on top of these platforms – using traditional programming languages such as C++, Java and Python – to serve various business, economic and government objectives. One of the most important of these technologies is the concept of “smart contracts”, which are self-executing contracts according to the terms of the agreement concluded between the seller and the buyer, which are written directly into lines of code.

In other words, a smart contract is an automated protocol that aims to facilitate the negotiation and implementation of contracts automatically. Smart contracts allow transactions to be completed and documented without the presence of third parties. Pairing the concept of smart contracts with blockchain technology is an important advantage because it is a decentralized system that exists between all parties who are allowed to participate or be seen, there is no need to pay for intermediaries, saves time, effort and resources as well as prevents human errors, and enables the parties to complete their transactions in the right place and time for them.

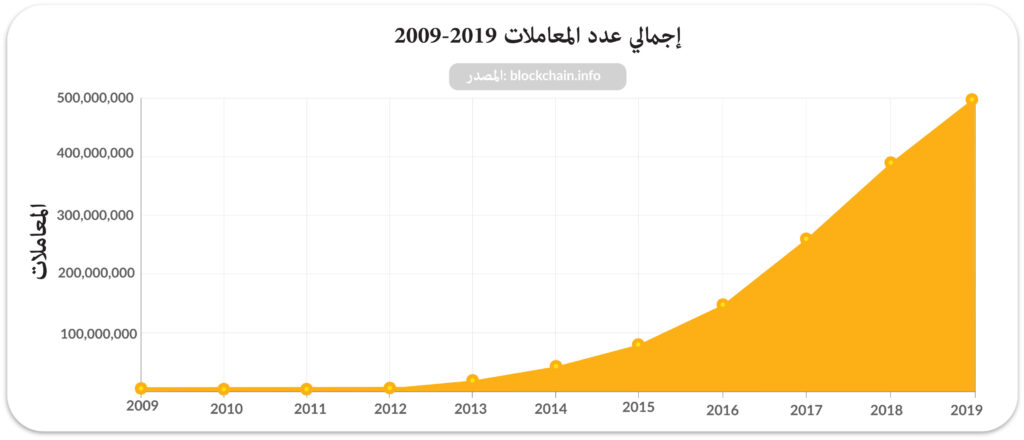

The Blockchain platform announced that the number of transactions in June of 2019 reached (430) million. It is reported that the first blockchain transaction was recorded in 2009, and during the first seven years, 100 million transactions were recorded. But it is noticeable in the last three years, that this number has increased by more than 100 million transactions every year.

The current statistics also indicate the increasing number of users of digital financial wallets on the Blockchain platforms, which currently amounts to about 40 million electronic wallets, noting that the number of subscribers during the first four years did not exceed five million subscribers, then the increasing volume of popular awareness of this technology and the number of subscribers to it to rise annually At a rate of ten million new subscribers annually.

All of this confirms a very large growth in the adoption of blockchain technologies, especially with the increasing interest of international institutions, and Europeans in particular, to adopt them in developing their services and products. International practices also indicate that this technology is able to provide features that are not provided by any other technology in electronic environments, such as transparency, security, tracking of transactions, increasing efficiency and speed of completion, and reducing costs.

Also, contrary to what many may imagine, that blockchain technology is related to encrypted digital currencies, researchers and experts believe that this is only a small part of its potential uses, as they point to unprecedented potential within the next few years, enabling revolutionary leaps In various economic and industrial fields that will touch the needs of institutions and individuals, and that what we see today is only the beginning!

| About | |

|---|---|

| Initiatives | |

| Knowledge | |

| Services | |

| Media Center | |

| Contact |